WARNING: Ignore this post at your own risk! Twenties are the time when life changes. Some are struggling to find a decent job and some are struggling to switch to a better position or company. A lot of graduates in India start preparing for government jobs – because of the pride attached to it or the job security or because they do not know what else to do. The struggle has just begun and life has hit hard.

When you finally get settled, you think everything is fixed now and you become ignorant. You start spending on things you craved and spend needlessly. Alcohol, parties, expensive clothes, mobiles, vacations, etc. eat away your salary. If this was not enough, our dear banks who think all the time about us and our financial well-being, give us huge offers on credit cards. Now with the comfort of the credit card, you start spending even more than your salary. After all, who the hell gives a damn about the financial future, it is the job of old and boring people who have nothing else to do!

You cannot be more wrong if you think like that. I can assure you of that. If you become financially aware and start planning early, the rewards will be enormous. So today I am going to share with you some financial decisions you can make in your twenties which will put you ahead in the game.

1. Live Below your Means

There is an old saying which says, ‘Cut your coat according to your cloth’. The simple meaning of this is to spend only what you can afford. Yet, we give in to our desires and buy things we cannot afford or that we do not need. Peer pressure and the ‘look rich among friends’ culture are destroying our youth. I read somewhere, “If your friends judge you by what phone you own, it’s time to get better friends, not a better phone.”

The habit of living below your means will pay you handsomely in times when you are in trouble. I am definitely not saying that you start saving on essential items like food and become a miser, but you must definitely think twice before buying a new phone or a bike or a new expensive purse, without which you can easily do.

Smart investors have the habit of saving or investing up to 50-60% of their income each month. I am sure saving that much is not for everyone but the point I am trying to drive home is that you must save at least 25% of whatever you earn.

The magical formula of saving

Saving a fixed sum of money faithfully each month is a difficult task. Some unplanned expense always seems to prevent us from saving regularly. We usually save what is left after spending. However, this approach is wrong. The correct approach for saving is to spend whatever is left after you set aside a fixed sum as savings. This method of saving is proven and successful people have been using it to inculcate discipline. I too use it and it has helped me save regularly.

Let’s take an example. Let’s say you earn Rs 30,000 monthly, and you decide to save 25% of your income, i.e. Rs 7,500 each month. All you have to do is to transfer Rs 7500 to a different saving account on the day your salary is credited to your account. If you do not have a separate savings account, open one as soon as possible. Just don’t think about this savings account and leave it alone at the month-end. You will develop a habit of saving over time.

2. Make an Emergency Fund

Problems do not call you before appearing. They appear out of nowhere at a time you expect them the least. While you cannot stop problems, you can mitigate their effect by being prepared. A sudden medical emergency or a job loss are some of the least expected events in life. It is for these unforeseen events that we must set aside a sum of money which is only for

Besides preparing you for emergencies, an emergency fund can come in handy if you want to leave your job to start a business, etc. Stop thinking, “It will not happen to me” or “It cannot happen to me”, these are the most harmful thoughts you can have.

Last year Larsen and Toubro (L&T), India’s biggest Engineering firm fired 14,000 employees. Layoffs are not uncommon these days and it is best to be prepared. An Emergency fund is a sum of money that you set aside for handling emergency situations such as listed above.

How big should be my Emergency fund?

Experts say that an emergency fund must be equal to a minimum of your six months salary. The recommended ideal size is equal to one years’ salary. So in case of a sudden financial crisis, you can fall back on your emergency fund to support yourself and your family. An emergency fund also helps you if you want to leave your job to start a business or something. It can be very relieving to have a backup in those times.

It is important to make sure that your emergency fund must be readily available. You should be able to access it at any time. Keep it in a savings bank account or as cash in your home safely. Do not invest it such that it gets locked for some time.

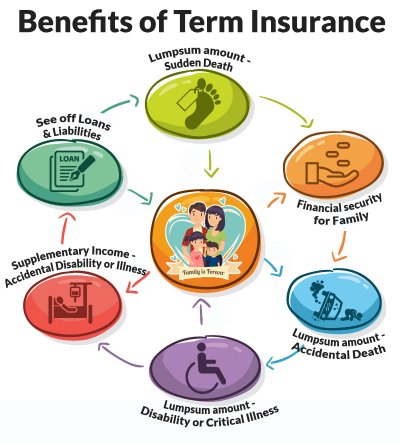

3. Get a Health Insurance and a Term Insurance

Learning from our mistakes is good, but it is always smarter to learn from others’ mistakes. This is so because some mistakes can cost your life. The Healthcare sector in India is extremely underfunded and this is why we turn to private hospitals in emergencies. Most of us are unprepared for medical situations which can cost a fortune. A one-week admission in a private room in a private hospital can easily set you back 1-10 lakhs depending on which hospital you are in. If the case is serious, much more might be needed.

India is not a wealthy country. 1 lakh is still much for many of us. If you think that you will never fall ill, please wake up. The probability that you will never need to get admitted

What is a term Insurance and why should I care about it?

Term insurance is a great way to provide for your loved ones in the unfortunate event you lose your life. Term insurance is essentially life insurance that gives you a relatively large cover for a small premium. It is very cheap compared to traditional life insurance plans and gives you a large cover(Generally 15 times your annual salary). If you have

In the unfortunate event of your death(don’t be scared, we’ll all die one day), the nominee gets the insured sum of money. For instance, a 1 crore cover is usually available for a yearly premium of Rs 6 thousand onwards. However, keep in mind that this premium is usually not returned in case the policyholder survives (some policies return it though). Regular life insurance policies such as those from LIC, offer some part of your premium back when the policy expires. It may seem like a smart choice to get your premium back in case you survive, but there’s a catch. The sum insured on death(cover) is about 5-8 times less than that offered by a term plan with a similar premium. So don’t confuse insurance with investment and choose wisely.

4. Be Cautious with Credit and Credit Cards

Banks offer benefits on credit cards because they know that most users will not pay back on time and will end up paying huge interest (up to 45% per annum – insane!). Credit cards are therefore not meant for everyone. They can easily spoil you if you do not have control over your impulses which force you to get instant gratification. If on the other hand, you are wise (like me 😛 ), you can use them to your benefit and avoid any late charges. You can read my article on how to smartly use your credit cards here: 10 smart hacks to get the most out of your credit card

5. Develop multiple Income streams and Invest money

Someone has truly said, “Aim for the best, but prepare for the worst”. If your source of income is only one, you are completely dependent on that source for your livelihood. If anything happens to that source, you will be helpless. That is why the most successful investors recommend you to develop multiple sources of income. They can be anything such as giving tuitions to kids, making money online from blogging, vlogging, selling items online or offline, freelancing, etc. If you look, opportunities are there. You just have to have a vision. This blog that you are reading is my part-time effort alongside a full-time job.

Another important point is to start investing money. Investing is not the same as saving. The goal of investing is to make money from money, to grow it without you putting any effort. In the words of famous author Robert Kiyosaki, by investing, you make money work for you. All rich guys (and girls too!) invest their money to grow it. Saving is good but don’t save everything. Invest a portion of your money to grow it.

Keeping money where it does not earn interest only reduces its value. Let me tell how. Suppose you save Rs 1000. The annual inflation rate is, say 6%. In the next year, your 1000 will become 940. The one thousand cash will still be with you but its purchasing power will have declined. In 2005, the price of milk was approximately Rs 17 per liter in India. It is now 3 times as expensive at Rs 54 per liter. Hope the point is clear.

The best Investment you can make

The best investment you will ever make is in your mind and body. By investing in your mind, I mean broadening your vision, learning from the experiences of others. This is only possible by continuously educating yourself. Read books and if you are not in the habit of reading, develop it because it will pay you immensely in the future. Leaders are readers, remember this. Listen to podcasts, attend seminars or watch them online.

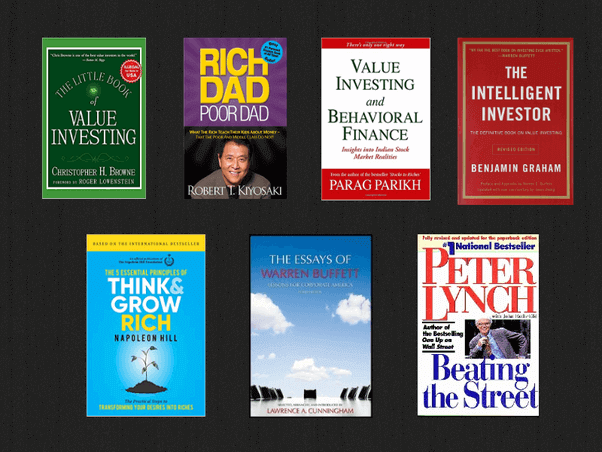

Some super marvelous books on investing I have read and which you must read too are Rich Dad Poor Dad by Robert Kiyosaki, The Intelligent Investor by Benjamin Graham, One up on Wall Street by Peter Lynch, and Money Master the Game by Tony Robbins. These are some of the finest books on investing. If you read these, I bet you will be smarter than 99% of people in this country when it comes to money. If you cannot afford to buy them, you can download them as pdf copies online. A great website is www.b-ok.xyz which you can try to find e-books. Nevertheless, satisfaction from a physical copy cannot be replaced.

By investing in your body, I mean your health. Keep yourself healthy. Exercise regularly, eat lots of fruits in the morning as breakfast. Eat whole fruits, don’t go for juices, they instantly spike insulin which is bad. Avoid alcohol. Quit smoking, it is your passport to hell. Have a good and complete sleep, buy a comfortable mattress, it is an investment. Buy a pair of UV-protecting sunglasses. Avoid social media and useless random content. It is fine if you are not active on Facebook or Instagram. I only use these to stay in touch with my friends or to share my blog posts.

Let me know if you learned something new from this post and please share your valuable comments, thoughts, recommendations, or suggestions. Share this with someone who requires to read this post. And thank you for reading!

{kind=link}